Sales Commission Amortization under ASC 606: How Visdum Helps

TL;DR

ASC 606 commission amortization is not a documentation problem. It is an operating model problem. The real decision is not which capitalization rules to apply, it is whether your finance team can sustain those rules across 200+ contracts, mid-cycle modifications, and a clawback policy that fires monthly. Spreadsheets handle the first 20 contracts. Purpose-built tools handle the next 2,000. The piece below covers what to evaluate when you decide to make the switch.

Key Takeaways

- The hardest part of ASC 606 commission amortization is not the math. It is sustaining the math when deals, plans, and clawbacks all change quarterly.

- Most teams overestimate how long they can run this in spreadsheets and underestimate how much migration debt accumulates while they wait.

- SDR spiffs misclassified as capitalizable is the single most common audit finding in this area. They are period costs, not contract acquisition costs.

- What starts as a finance reporting issue becomes a fundraising and audit issue. Bad commission amortization shows up first in quarter-end close cycles, then in M&A diligence drag, then in audit scope expansion.

- High-performing finance teams treat ASC 606 amortization as a continuous data pipeline, not a quarterly project. The companies winning M&A processes in 2026 produce audit-ready commission schedules on demand.

- Generic ICM tools added ASC 606 compliance as a reporting layer. ASC 606-native platforms were architected around the standard. Those are different products with different long-run cost profiles.

Every SaaS CFO who has been through an audit cycle knows the same story. The technical question about ASC 606 commission treatment takes an afternoon. The operating model that sustains the technical answer across a fiscal year takes years to get right.

The real decision is not which capitalization rules apply to your commission plan. The standard is clear on that. The real decision is whether the system you use to apply those rules can survive 200+ contracts, mid-cycle modifications, multi-currency entities, and a clawback policy that fires every month.

This guide covers what ASC 606 requires for sales commissions, where spreadsheets break in practice, what purpose-built tools actually do differently, and how to evaluate whether you have outgrown your current approach. Technical depth on the standard itself lives in the linked pieces. This is the operational walkthrough.

What does ASC 606 actually require for sales commissions?

ASC 606, through its companion subtopic ASC 340-40, requires sales commissions that qualify as incremental contract acquisition costs to be capitalized as deferred assets and amortized over the period the customer benefits.

Three conditions must be met for capitalization:

- Incremental: the commission would not have been paid without winning the contract. This is where most audit findings cluster. SDR spiffs paid per meeting fail this test because they pay regardless of whether the deal closes.

- Recoverable: the company expects to recover the cost through future revenue. Heavily discounted or short-term deals can fail this test, but the failure is rare in healthy SaaS pricing.

- Period of benefit exceeds one year: the practical expedient lets companies expense commissions when amortization would be 12 months or less. Useful, but not the escape hatch most teams want it to be.

For the deeper treatment, see the ASC 606: What is it? pillar guide ASC 606 Revenue Recognition for SaaS. For the period-cost question specifically, see Is Sales Commission a Period Cost?.

Why do spreadsheets break at ASC 606 commission amortization?

Every spreadsheet works until it does not. The failure curve is non-linear: gradual for the first 20 to 50 contracts, then sharply degraded as complexity compounds. Five forces drive that breakdown:

- Mid-cycle modification math compounds quickly. Multi-year deals, renewals at different commission rates, expansion adds, and product swaps each require schedule recalculation. By contract 100, the conditional logic in your sheet is unauditable.

- Clawback tracking becomes the bottleneck. Every churn requires manually identifying the unamortized balance, reversing it on the balance sheet, and reconciling against revenue. By 100 contracts, this is hours per week. By 500, it is a full-time job.

- Finance and RevOps maintain different copies. Sales operations exports commission data, Finance reformats it for ASC 606, and the two versions drift over time. Disputes become irresolvable because nobody knows which copy is right.

- Plan changes force structural rebuilds. A new commission structure or rate change forces redesign of the spreadsheet. Historical schedules need to be preserved, projected schedules need to be reissued.

- Audit prep takes weeks of forensic work. Producing capitalized commission schedules, amortization waterfalls, and clawback logs from manual sheets means reconciliation against every contract, every commission, every period.

Most teams underestimate when the breaking point arrives. The pattern: "this works for now," repeated quarterly, until a controller leaves and the next person inherits a spreadsheet they cannot defend in an audit. By then the migration cost includes not just the data but the policy archaeology required to reconstruct what the old sheets actually meant.

The Hidden Cost

What starts as a reconciliation issue in Q1 becomes an audit finding in Q4. What looks like a commission accounting error becomes an enterprise audit scope expansion: once auditors lose confidence in commission treatment, they typically expand scope to revenue recognition, contract management, and disclosure controls. The cost is rarely the commission error itself. It is the expanded audit hours, the delayed close, and the management letter that follows.

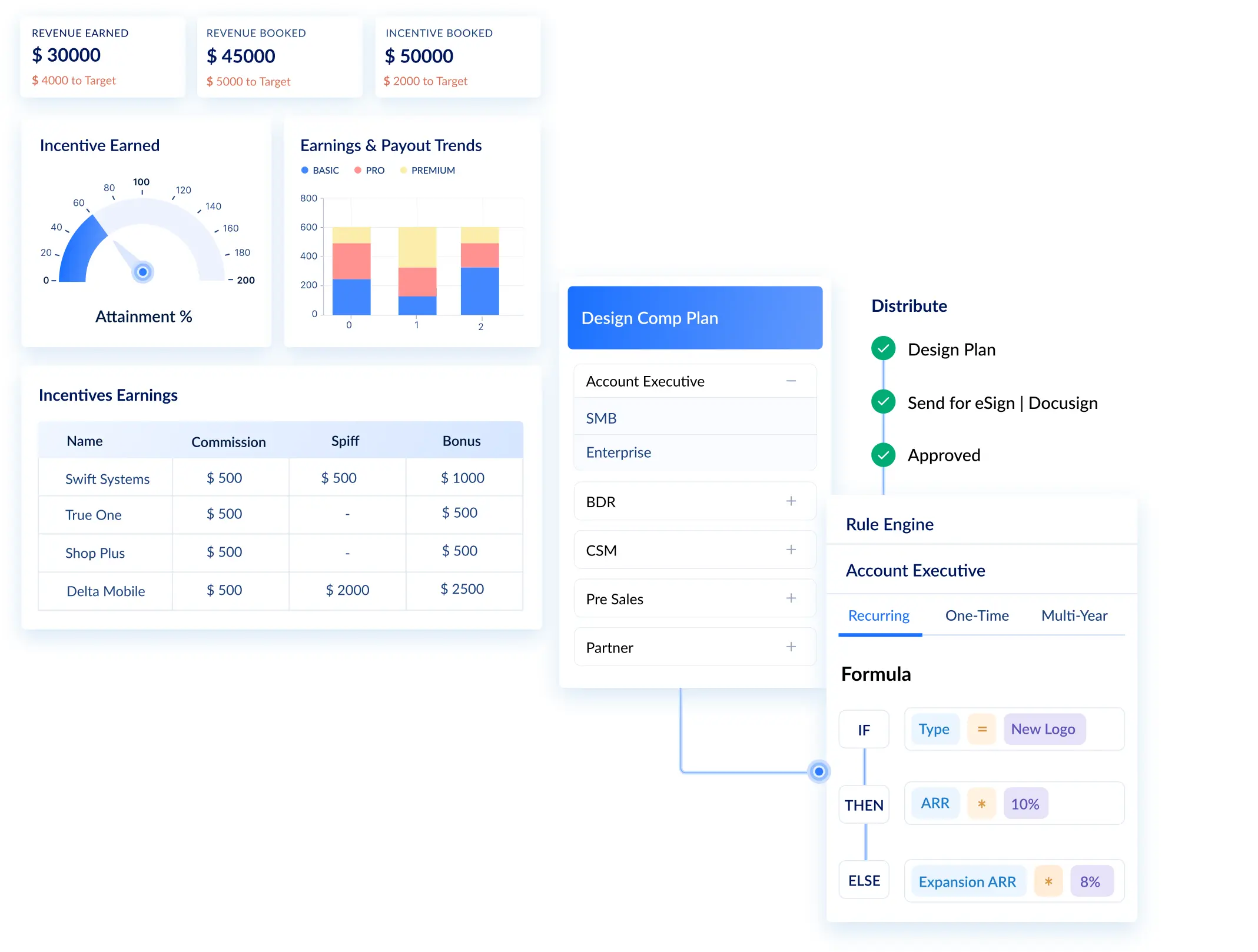

How does Visdum handle ASC 606 commission amortization?

Visdum was built specifically for sales compensation under ASC 606. The architecture matters here. Generic ICM tools added ASC 606 reporting as a layer on top of commission calculation systems built for the pre-ASC 606 world. Visdum was architected around the standard from day one, which means amortization is part of the daily operation, not a quarterly export.

The workflow runs in five continuous steps. Each is configured once, then runs in the background.

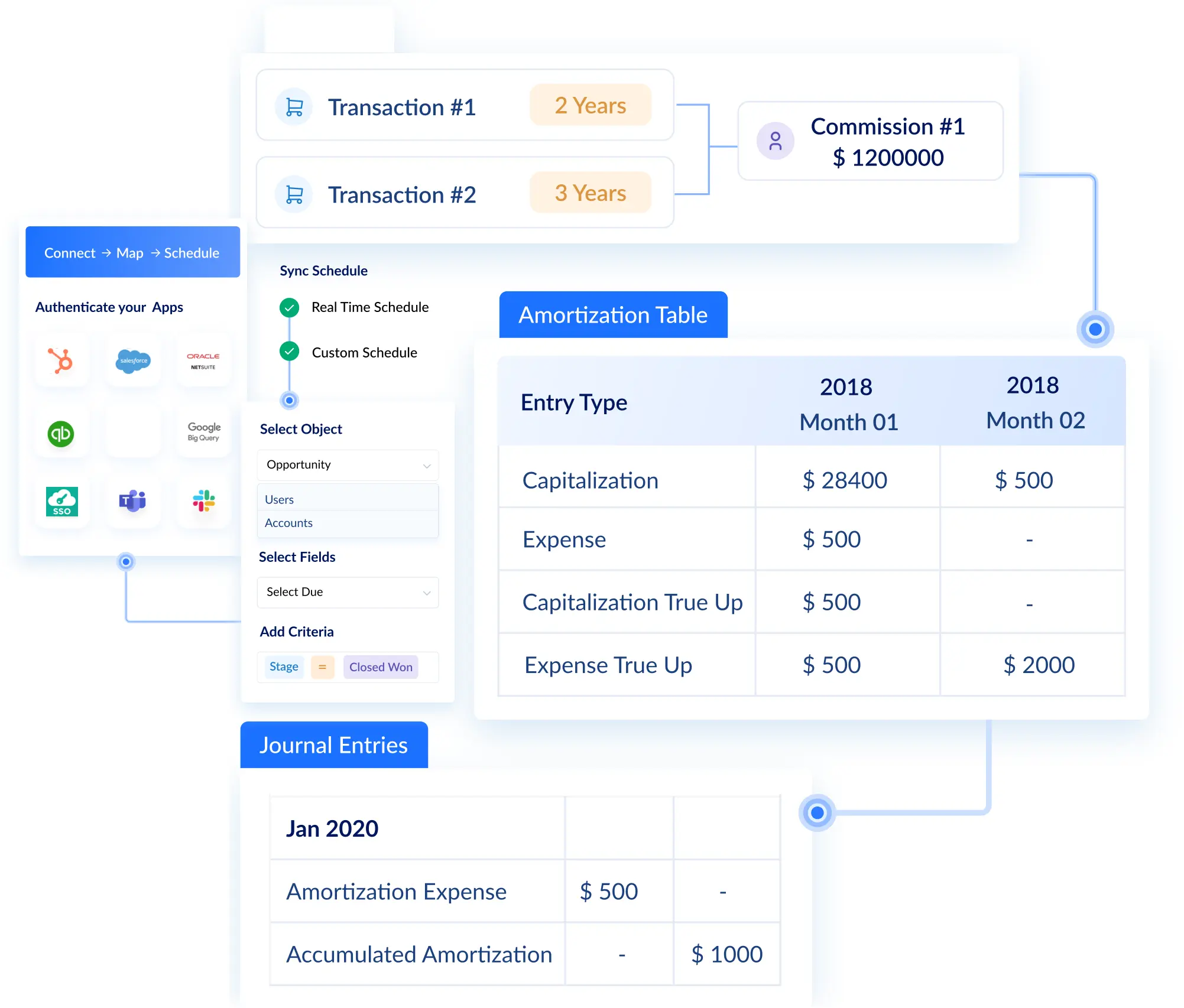

Step 1: Sync commission and contract data

Visdum integrates with your CRM, billing system, and HRIS to pull commission payments and link them to the underlying contracts. Every commission has a direct connection to the contract that earned it, the rep who closed it, and the revenue period it supports.

Why this matters: the audit-defensible part of ASC 340-40 is not the capitalization math. It is the contract linkage. Auditors test whether every capitalized commission can be traced to a specific revenue contract, with full lineage. Spreadsheets typically lose this lineage during data manipulation. Direct sync preserves it.

Step 2: Identify which commissions qualify for capitalization

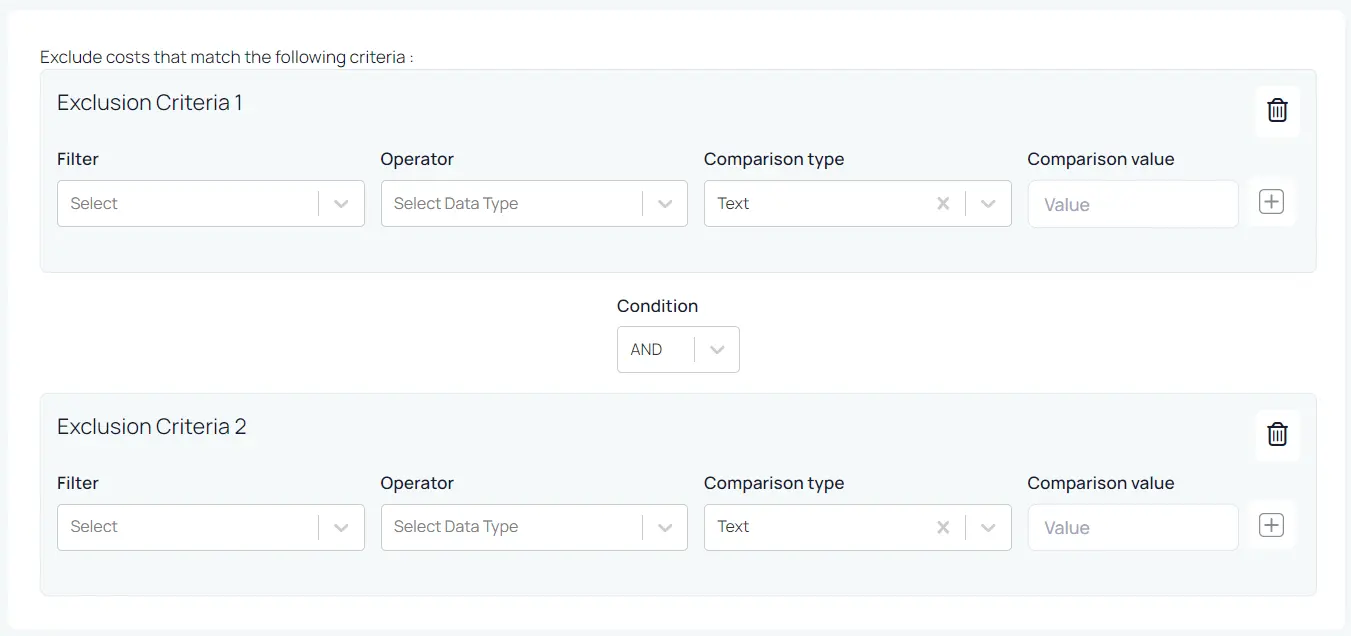

Define your capitalization criteria once: which roles, which deal types, which commission components. Visdum then automatically flags every new commission against those rules, separating capitalizable AE commissions from expensable SDR spiffs and BDR meeting fees.

Why this matters: inconsistent classification is the single largest source of audit findings in this area. When the rules live in a policy document and the application lives in a spreadsheet, the two drift. Rules-based classification at the data layer means every commission gets the same test, every time, regardless of who entered it.

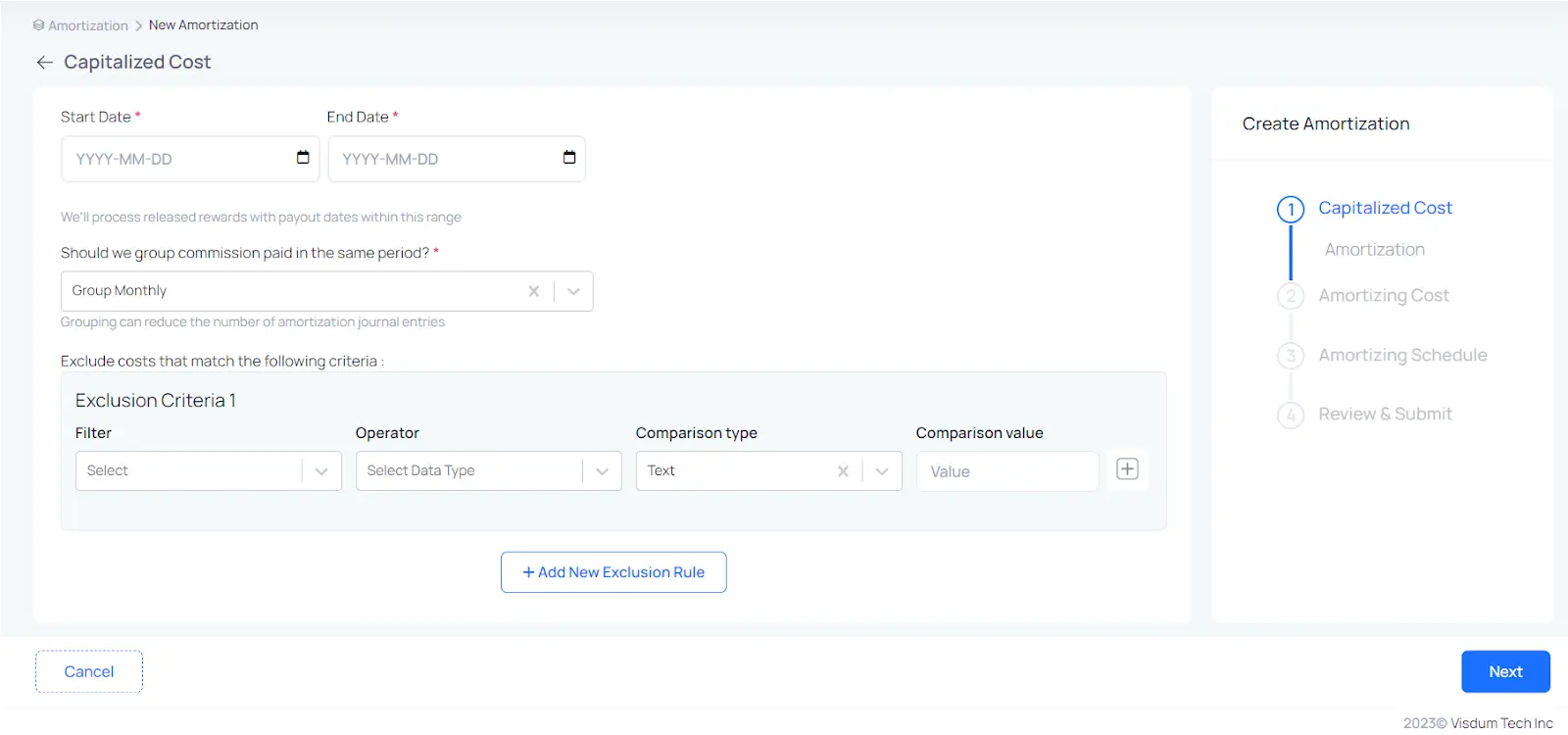

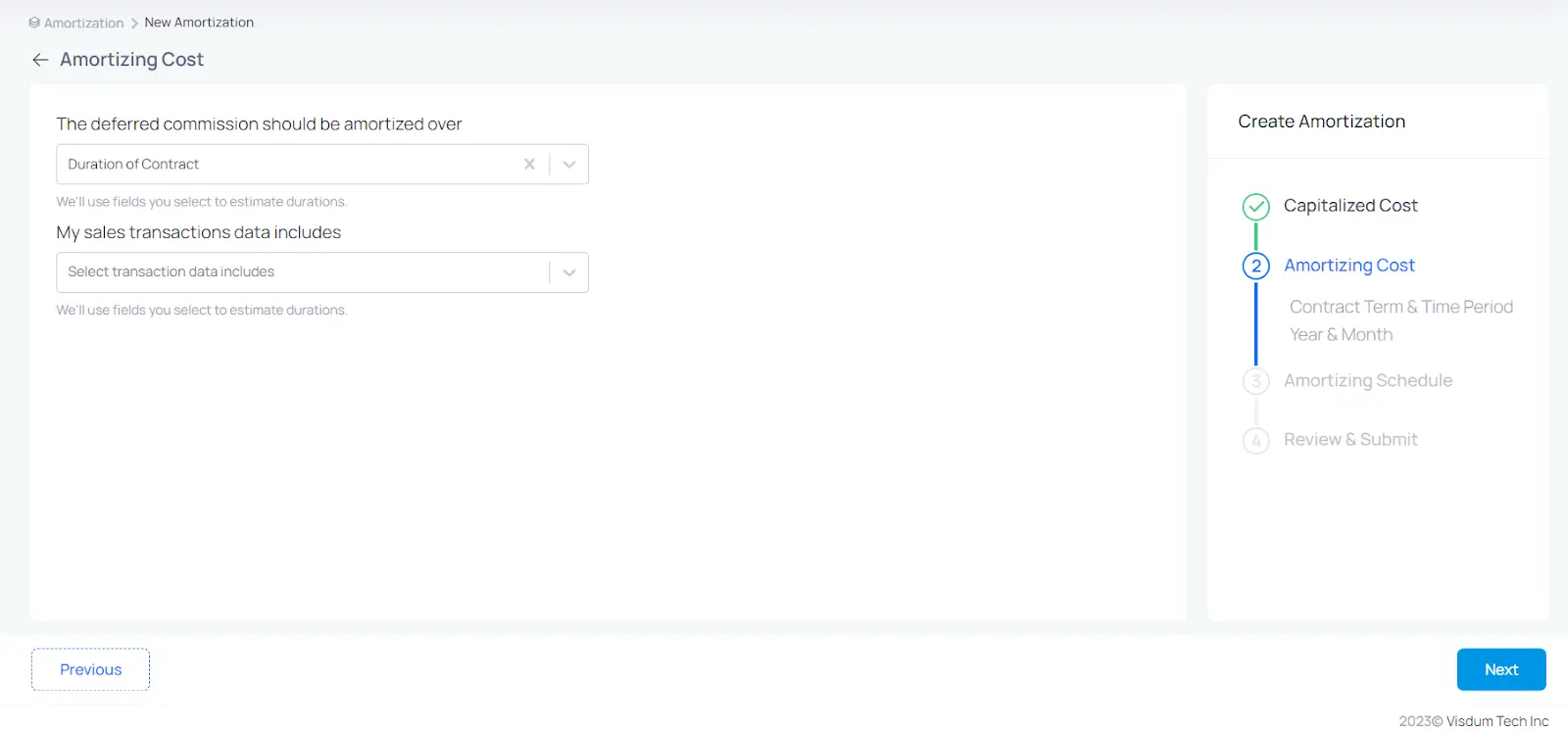

Step 3: Set amortization rules and periods

Choose whether to amortize over the initial contract term or the expected customer life. Configure different amortization periods by role, region, or product. Visdum supports one-year, three-year, five-year, and custom periods, with full historical documentation of the rationale for each choice.

Why this matters: the amortization period is the most audit-scrutinized decision in ASC 340-40. Auditors will ask why you chose 36 months over 12, and the answer must be supportable with renewal data. Visdum stores both the choice and the supporting data, so the answer is in the system, not in someone’s head.

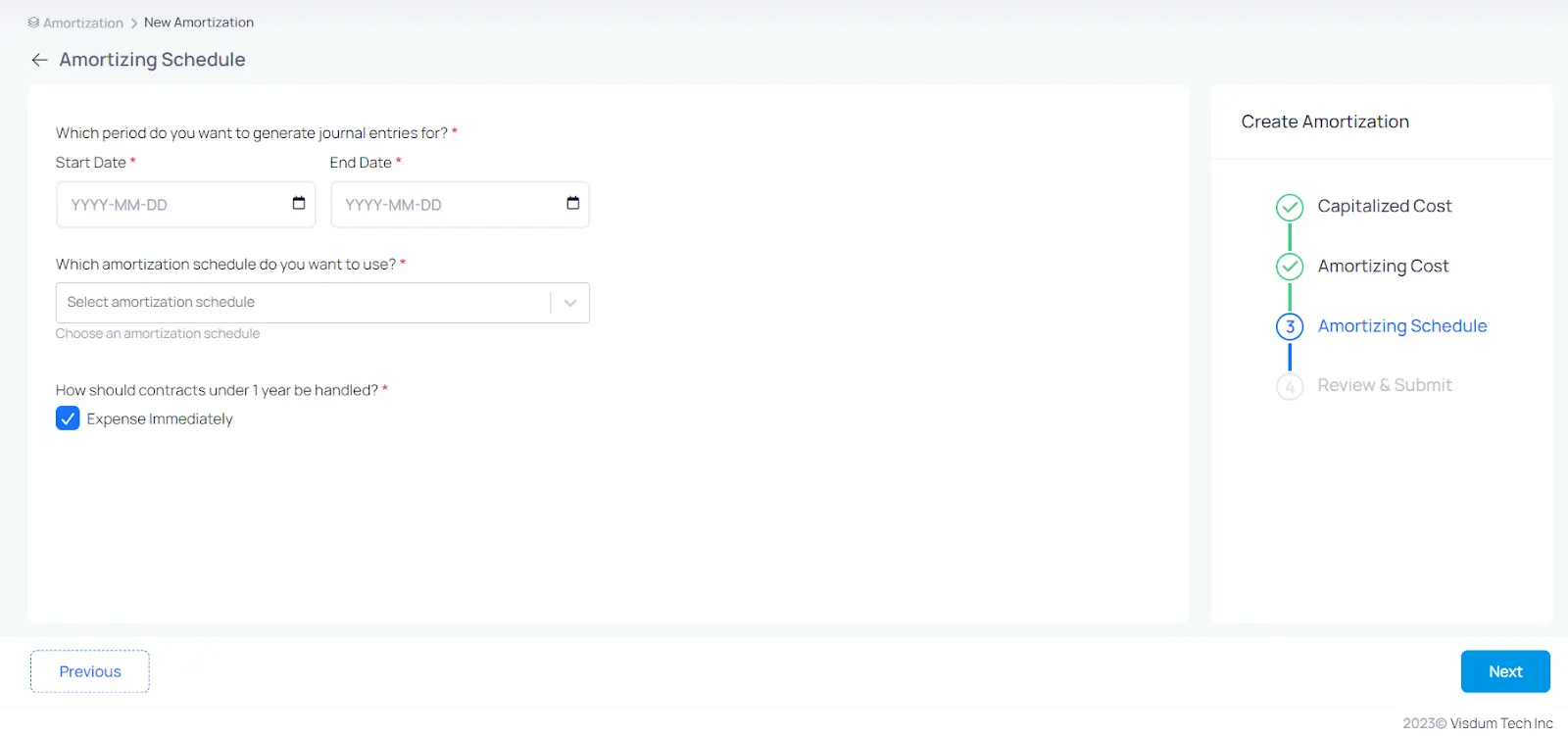

Step 4: Generate amortization schedules continuously

Once rules are set, Visdum generates monthly amortization schedules automatically against every capitalizable commission. The Waterfall report provides transaction-level visibility: amount amortized each period, cumulative amortization, remaining balance. Schedules update in real time as new commissions land or existing contracts get modified.

Why this matters: continuous schedules change the close cycle. Finance teams stop generating amortization at quarter-end and start reviewing it. The work shifts from production to oversight, which is where finance leaders actually want their team operating.

Step 5: Track clawbacks and produce audit-ready reports

When a customer churns, downgrades, or cancels, Visdum reverses the unamortized commission balance automatically against the revenue contract. Clawback logs, capitalized commission schedules, and policy documentation are produced on demand.

Why this matters: Clawback handling is what breaks most spreadsheet operations first. Each churn requires identifying the deferred asset balance, reversing it, and tying it back to the revenue contract. Automate the reversal, and the largest source of monthly finance friction in this area disappears.

The Maturity Signal

High-performing finance teams in 2026 do not produce ASC 606 commission reports at year-end. They produce them continuously. The audit at year-end is then a review of work already done, not a sprint to compile it. This is the operating model investors and acquirers want to see during diligence.

What audit-ready commission amortization actually produces

Four artifacts show up in every well-run ASC 606 audit. The difference between teams that pass cleanly and teams that get findings is not whether they produce these. It is whether they produce them on demand from a single source of truth or whether they reconstruct them from spreadsheets each quarter.

| Report | What it shows | What sloppy versions miss |

|---|---|---|

| Capitalized Commissions Schedule | Every capitalized commission, amortization period, balance | Contract linkage and rationale for amortization period choice |

| Amortization Waterfall | Transaction-level monthly amortization | Reconciliation back to revenue period; cumulative balance accuracy |

| Clawback and Impairment Log | Each churn, downgrade, cancellation, asset adjustment | Tying reversals back to the originating contract; impairment vs reversal classification |

| Policy Documentation | Capitalization criteria by role, amortization methodology | Version history of policy changes and supporting data for amortization period assumptions |

Model your own scenarios with the ASC 606 Amortization Calculator, or download the ASC 606 Sales Commission Amortization Template for a manual baseline.

How does Visdum compare to spreadsheets and other ICM tools?

Three options to operationalize ASC 606 commission amortization. The honest comparison is not about feature checkmarks. It is about which option holds up under the operating conditions of a growing SaaS finance team.

| Dimension | Spreadsheets | Generic ICM tools | Visdum |

|---|---|---|---|

| Origin story | Built for one-off modeling, not multi-year compliance | Built before ASC 606 mattered; compliance added as a reporting layer | Built ASC 606-native from foundation |

| Time to first audit-ready report | Weeks of forensic reconciliation each quarter | Days; depends on data quality and connector reliability | On demand once configured |

| Effect on close cycle | Adds 5 to 10 days at quarter end | Reduces but rarely eliminates the bottleneck | Removes commission amortization from critical path |

| Clawback handling | Manual reversal entries; days per churn; deferred asset drift accumulates | Partial automation; often requires manual reconciliation to revenue | Automatic reversal linked to revenue contract |

| Adapts to plan changes mid-year | Structural rebuild required | Possible but typically professional services engagement | Versioned plans; new commissions follow new rules from effective date |

| Audit finding history (industry pattern) | Findings on inconsistent classification and broken contract linkage | Findings on disclosure completeness and lineage gaps | Designed to pass without findings |

| Real cost over 3 years | Hidden in finance team headcount and audit hours | Per-payee licensing plus integration costs plus implementation services | Predictable; payback typically within first year for teams above 50 reps |

Spreadsheets work for teams below 20 reps and simple plans. Generic ICM tools handle commission calculation well but treat ASC 606 as an output, not an architecture. ASC 606-native platforms make the compliance work happen automatically, which means the finance team stops being a production line and starts being a review function. That shift is what mature SaaS finance organizations are buying.

Common implementation pitfalls and how to avoid them

Most teams approach the switch from spreadsheets like an IT migration. It is not. It is a policy migration that happens to involve software.

| Pitfall | Why it actually breaks deployments | The fix that works |

|---|---|---|

| Migrating spreadsheets without cleaning data first | Errors carry forward into the new system, audit findings repeat | Run a data audit before migration; document known issues and treatment |

| Treating implementation as IT-only | Finance and RevOps stay misaligned on policy interpretation | Joint Finance + RevOps + Sales Ops kickoff before configuration starts |

| Skipping the policy documentation step | System captures the math but loses the rationale | Document capitalization criteria by role and amortization period rationale before going live |

| Migrating only current contracts, no historical schedules | Year-over-year reporting breaks at the implementation date | Migrate at minimum the prior fiscal year; ideally two years |

| Underestimating change management for reps | Adoption slow because reps still trust their old spreadsheet views | Train reps on new commission visibility first; the trust dividend funds finance adoption later |

Most teams overestimate the technical work and underestimate the policy work. The configuration is fast. The capitalization policy that holds up under audit is slow. Budget your time accordingly.

TL;DR

The switch from spreadsheets to a purpose-built ASC 606 platform is less about replacing software and more about replacing an operating model. The decision pays back when the finance team stops producing schedules and starts reviewing them, when audits become reviews rather than projects, and when M&A diligence finds clean financials waiting.

FAQ: ASC 606 commission amortization in practice

How long does implementation typically take?

Four to eight weeks for most mid-market SaaS companies, twelve weeks for enterprise rollouts with multi-region plans. The variable is rarely the software. It is the upstream data quality and the time required to align Finance, RevOps, and Sales Ops on capitalization policy. Teams that try to compress this typically pay for it in rework after go-live.

Does Visdum integrate with our existing CRM and billing system?

Yes, with the major SaaS finance and revenue tools. Two-way sync ensures commission data, contract data, and clawback events stay reconciled. The thing to test during evaluation is not whether an integration exists, but how it handles edge cases: deleted records, retroactive contract changes, and currency conversions. These are where weaker connectors fail.

How does Visdum handle commission plan changes mid-year?

Plan changes are versioned. New commissions follow new rules from the effective date forward. Historical schedules remain intact and continue to amortize under the rules in force when they were created. The version history is what auditors will ask to see when policy has changed.

What happens to existing amortization schedules during migration?

Visdum supports importing historical schedules and continuing them on the existing amortization curve. Most teams migrate the prior 12 to 24 months. Going further back is technically possible but rarely worth the data archaeology required.

Does Visdum support multi-entity and multi-currency operations?

Yes. Multi-entity consolidation, multi-currency commission payments, and entity-specific policy documentation. The audit-defensible part is keeping policy variations explicit. Common mistake: applying one policy globally and then disclosing variation as a footnote. The better pattern is configuring per-entity policy and producing consolidated reporting from there.

How does pricing typically compare to spreadsheets or other ICM tools?

Spreadsheets look cheap on the procurement spreadsheet and expensive on the finance team’s calendar. ICM tools are typically priced per payee, which scales unpleasantly with rep growth. Visdum pricing is structured around the operating problem rather than headcount. The total-cost-of-ownership comparison usually breaks in our favor above 50 reps, and the audit-risk reduction is the part that does not show up in either pricing model but matters most.

See ASC 606 commission amortization in action

You do not need a calculator. You need a system that calculates. The fastest way to evaluate whether Visdum fits is to see it running on real commission data:

- Book a personalized demo to walk through your specific commission scenarios with the team.

- Try the ASC 606 Amortization Calculator to model amortization on your own contracts.

- Explore the product tour to see the workflow on sample data.

Visdum works to your sales compensation process as flexible enough to respond quickly to market changes, without worrying about wrong calculations or payment delays.