ASC 606 Sales Commission Amortization Reporting Template

Download Free Template

Who should use this template?

This template and instructions are designed for:

- Finance and accounting professionals in SaaS (Software as a Service) companies

- Businesses that need to comply with the ASC 606 revenue recognition standard

- Companies with significant sales commission expenses that need to be amortized over contract durations

What is ASC 606?

ASC 606 is the Accounting Standards Codification (ASC) Topic 606, which deals with revenue recognition from contracts with customers. It was introduced to standardize how companies recognize revenue across industries and capital markets.

One key aspect of ASC 606 that's relevant to this template is how it treats sales commissions.

Under ASC 606, sales commissions are often considered costs of obtaining a contract. Instead of expensing these costs immediately, they are capitalized and then amortized (spread out) over the life of the contract or the expected customer relationship.

This is done to better match the timing of these expenses with the revenue they help generate.

About the ASC 606 Sales Commission Reporting Template

The ASC 606 Amortization Schedule Template is designed to help manage sales commission expenses under the ASC 606 accounting standard.

Instead of recognizing the full commission as an expense when it's paid, ASC 606 often requires spreading it out over time to match it with the revenue it helps generate. This template automates these calculations.

Let's look at how this works using examples from the template:

Commission Calculation

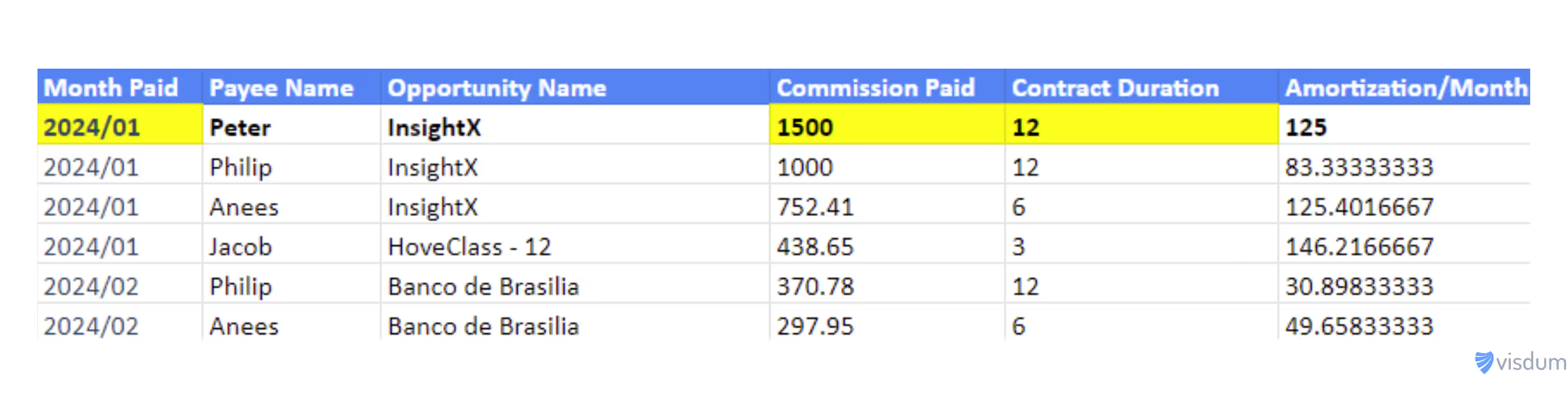

In the "Granular Amortization" sheet, we see that in January 2024, Peter earned a commission of $1,500 for a 12-month contract with InsightX.

Instead of expensing the full $1,500 immediately, the template calculates a monthly amortization amount by dividing the total commission by the contract duration:

$1,500 / 12 months = $125 per month.

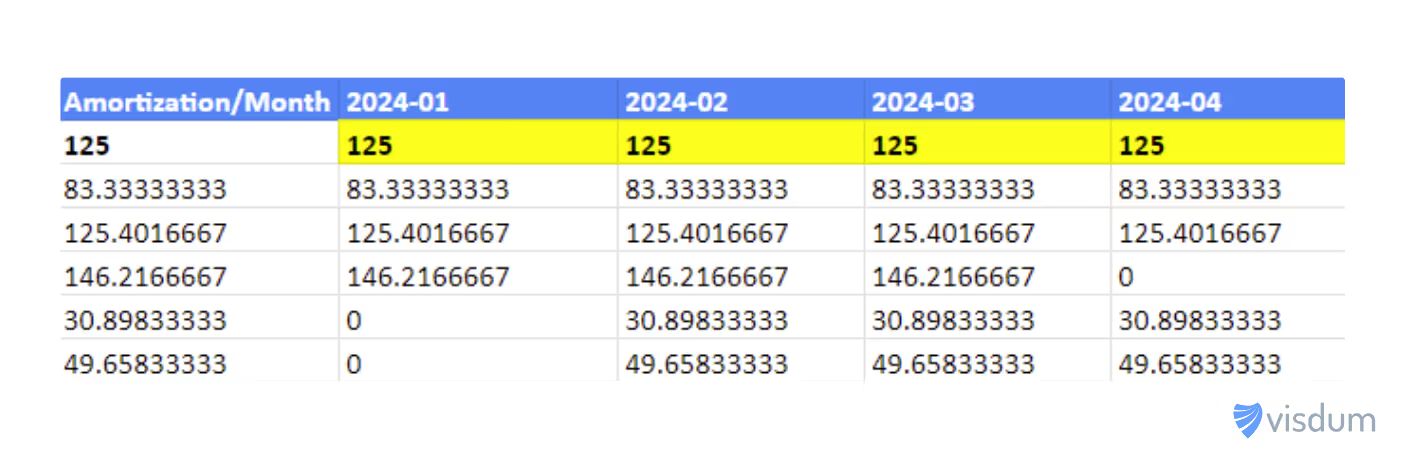

Amortization Spread

The template then spreads this $125 across 12 months, starting from January 2024.

You can see in Peter's row that there's a $125 entry in each month from January 2024 to December 2024.

Multiple Commissions

In the same month (January 2024), we see that three other commissions were also paid:

- $1000 to Philip (12-month contract),

- $752.41 to Anees (6-month contract), and

- $438.65 to Jacob (3-month contract).

The template calculates the monthly amortization for each and spreads them across their respective contract durations.

Cumulative Amortization

In the "Cumulative Amortization" sheet, we can see how these individual amortizations add up.

For January 2024, the total amortization amount is $479.95.

This is the sum of the monthly amortizations for all four January commissions

($125 + $83.33 + $125.4016667 + $146.2166667).

Notice how this amount changes over time:

- It stays the same for February and March.

- In April, it drops to $333.735 because Jacob's 3-month contract ended.

- In July, it drops further to $208.33 because Anees's 6-month contract ended.

- From January 2025, it becomes zero because all contracts from January 2024 have ended.

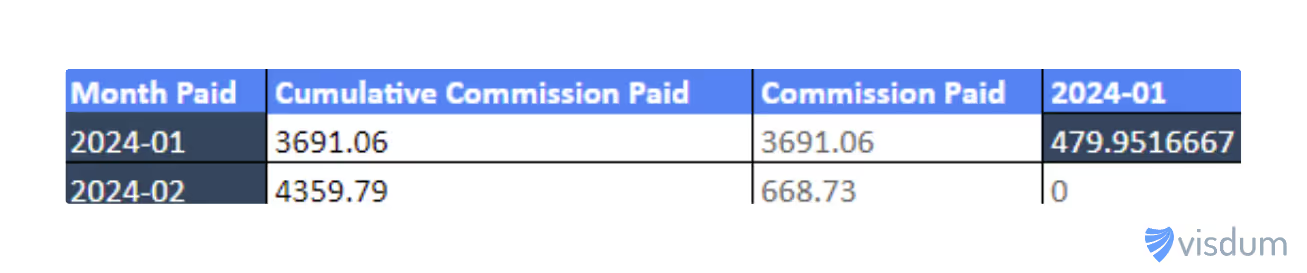

Deferred Commission

The "Deferred Commission (Monthly)" sheet shows how much of the commission remains to be expensed.

In January 2024:

- Total commission paid was $3,691.06.

- The amortized (expensed) amount was $479.95

- This leaves a deferred commission balance of $3,211.108

By December 2024, even though no new commissions were added in this example:

- The cumulative paid commission remains $4,359.79.

- The cumulative amortized commission reaches $4,328.891667.

- The deferred commission balance drops to just $30.89833333. This small remaining amount is what's left to be amortized in January 2025 from Philip's 12-month Banco de Brasilia contract (which started in February 2024).

The Power of the Template: Imagine manually calculating these figures for dozens or hundreds of commissions, each with different payment dates and contract durations.

This template automates that process. When you input a new commission in the "Granular Amortization" sheet - say, changing Peter's commission to $2,000 - all the subsequent sheets automatically update their calculations.

The key idea remains that instead of recognizing the full commission as an expense when it's paid, you spread it out over time. This template makes that process manageable, ensuring that expenses are recognized in the appropriate periods and aligned with the underlying contracts and revenue recognition.

It provides a clear, month-by-month view of how much commission expense should be recognized, how much has already been recognized, and how much remains to be recognized in the future.

How to use this template (step-by-step)

Open the ASC 606 Sales Commission Reporting Template and navigate to the "Granular Amortization" sheet. This is the only sheet where you'll need to enter data.

Entering Commission Details

In the first available row, enter the following information for each sales commission earned:

- Month Paid: The month when the commission was paid (use the format YYYY/MM, e.g., 2024/01 for January 2024).

- Payee Name: The name of the sales representative who earned the commission.

- Opportunity Name: The name or identifier of the deal or opportunity.

- Commission Paid: The total commission amount paid for that deal.

- Contract Duration: The duration of the contract in months.

If you have multiple commissions in the same month, enter each commission on a separate row.

Automatic Calculations

- The template will automatically calculate the monthly amortization amount by dividing the commission paid by the contract duration.

- The calculated amortization amount will be spread out across the corresponding monthly columns, spanning the contract duration.

- The "Cumulative Amortization" sheet will update to show the total amortization balance for each month, summing up the individual amortization amounts from the "Granular Amortization" sheet.

- The "Deferred Commission (Monthly)" sheet will calculate the remaining balance of commissions to be amortized (deferred) in future periods, based on the amortization schedule.

Adding More Rows or Extending the Time Period

- If you need to add more rows to the "Granular Amortization" sheet, simply insert new rows below the existing data, following the same format and column headers.

- The template currently displays amortization balances until the end of 2028. To extend the amortization schedule beyond 2028, add new columns to the "Granular Amortization" sheet, following the same pattern as the existing columns.

- The "Cumulative Amortization" and "Deferred Commission (Monthly)" sheets will automatically update their calculations to include the new time periods, as long as the column headers in the "Granular Amortization" sheet are updated accordingly.

How does this template help your SaaS business?

Understanding the business impact of using this ASC 606 amortization template is crucial, especially for SaaS (Software as a Service) businesses. Let's explore how creating these reports translates into tangible business value:

Accurate Profitability Measurement

In SaaS businesses, customer acquisition costs (CAC), which include sales commissions, are significant. By using this template and amortizing commissions over the contract duration, businesses get a more accurate picture of profitability.

For example, let's look at the InsightX deal with Peter in January 2024.

The commission is $1,500 for a 12-month contract.

Without amortization, January's profit would be reduced by the full $1,500.

But with amortization, only $125 is expensed each month.

If the monthly revenue from this contract is, say, $1,000, the profit picture changes dramatically:

Without Amortization:

Month 1: Revenue $1,000 - Commission $1,500 = -$500 (Loss)

Month 2-12: Revenue $1,000 - Commission $0 = $1,000 (Profit)

With Amortization: Every Month:

Revenue $1,000 - Amortized Commission $125 = $875 (Profit)

This more accurately reflects that the business is profitable from day one, rather than taking a big hit in the first month.

Alignment with Customer Lifetime Value (CLV)

SaaS businesses focus heavily on CLV. By spreading commission expenses over the contract lifetime (or even expected customer lifetime), the template helps align expenses with the periods in which customer value is realized.

In our template, we see contracts ranging from 3 months (Jacob's HoveClass deal) to 12 months (several others). Each is amortized over its specific timeframe, matching expense recognition with value delivery.

Improved Sales Compensation Planning

The granular view provided by the template allows businesses to analyze the long-term cost of their sales compensation plans. They can see not just how much they're paying out now, but how those payouts will impact expenses in future months.

For instance, the template shows that despite no new commissions after February 2024, the business continues to recognize commission expenses until January 2025.

This foresight can be crucial for budgeting and cash flow management.

Better Investor and Stakeholder Communication

SaaS businesses, especially startups, often face scrutiny from investors regarding their unit economics. The amortization approach demonstrates that the company understands the long-term nature of its customer relationships and is accounting for costs accordingly.

When showing the "Deferred Commission (Monthly)" sheet to investors, a SaaS company can explain that while they paid out $4,559.79 in commissions by February 2024, they're recognizing these costs gradually.

This approach often resonates well with investors who appreciate seeing expenses matched with corresponding revenue.

Scalability and Predictability

As a SaaS business grows and acquires more customers, the number of contracts and associated commissions can become overwhelming. This template provides a scalable way to manage that complexity.

Moreover, it enhances predictability.

By looking at the "Cumulative Amortization" sheet, finance teams can forecast future expense levels even without new sales.

For example, they know that in June 2024, they'll have at least $430.96 in commission expenses from deals already closed, helping with more accurate financial projections.

Compliance and Audit Readiness

While not a direct business value, being compliant with accounting standards like ASC 606 is crucial. This template provides a clear audit trail, showing exactly how each commission is being amortized.

During audits or due diligence (like for fundraising or acquisition), having this level of detail readily available can save significant time and resources.

Decision Making on Contract Structures

The template can also inform decisions about contract structures. For instance, if the business notices that longer contracts lead to better expense spreading and more predictable financials, they might incentivize the sales team to push for longer commitments from customers.

Cash Flow vs. Profitability Insights:

Lastly, this template highlights the difference between cash flows and accrual-based profitability. While all commissions might be paid upfront (impacting cash), the accrual-based expense recognition is spread out. This insight helps managers understand that a month with high commission payouts isn't necessarily an unprofitable month from an accounting standpoint.

In conclusion, for SaaS businesses, where customer relationships extend over time and upfront costs are high, this ASC 606 amortization template isn't just about compliance.

It's a strategic tool that provides deeper insights into business economics, aids in better decision-making, supports meaningful stakeholder communications, and ensures that the company's financial story accurately reflects the recurring nature of its business model.

By matching expenses with revenue more precisely, it allows the business to see its true profitability trajectory, essential for sustainable growth in the SaaS world.

Get a Demo Customized to Your Sales Comp Plans